Real Estate APAC - Quarterly Spotlight

A renewed stretch of uncertainty, with an added dose of volatility

Global growth forecasts have been downgraded

- The global economy started 2025 with a sense of cautious optimism, but this has rapidly changed over the past few months as the world grappled with the ramifications of the mercantilist policies of the US administration and tariff volatility

- With the world facing an unprecedented level of uncertainty, global economic growth forecasts have been revised down – according to the International Monetary Fund (IMF) as of 4 April 2025, global growth is projected to drop to 2.8 per cent in 2025 and 3.0 per cent in 2026, down from 3.3 per cent for both years

- The macro-economic outlook for Asia has also weakened and growth for the region is projected by the IMF to slow to around 3.9 per cent and 4.0 per cent in 2025 and 2026 respectively, down from 4.6 per cent in 2024

- While the US Federal Reserve continued to extend its pause in its interest rate cut cycle at its May 2025 meeting, APAC’s easing cycle (with the exception of Japan) seemed to be in full swing amid concerns over the weaker growth outlook and trade uncertainties

What piqued our interest?

While there are indications that the rising macroeconomic uncertainty is impacting investment momentum with buyers steering away from cyclical sectors, there remain some silver linings

- Global real estate investment momentum hitting a snag. While geopolitical shifts and the tariff situation remain highly fluid, there are early indications that global real estate markets are starting to feel the heat – according to MSCI Real Capital Analytics (RCA), global investment volume was flat in Q1 2025 on a YoY basis, a sharp contrast after volume increased by close to 50 per cent YoY in Q4 2024

- APAC real estate markets drawn into the fray. Real estate investment activity in Asia Pacific (APAC) also took a beating, with Q1 2025 deal volume falling 45 per cent QoQ and 18 per cent YoY; the pipeline of pending deals also contracted from Q4 2024

- Rise in cross-border investments in APAC. Notwithstanding the weaker investment activity, cross-border investment into APAC commercial real estate continued to increase in Q1 2025, notably driven by inflows from outside the region – a considerable proportion of the capital came from investors based in North America, who have been recently been reigniting their focus in APAC

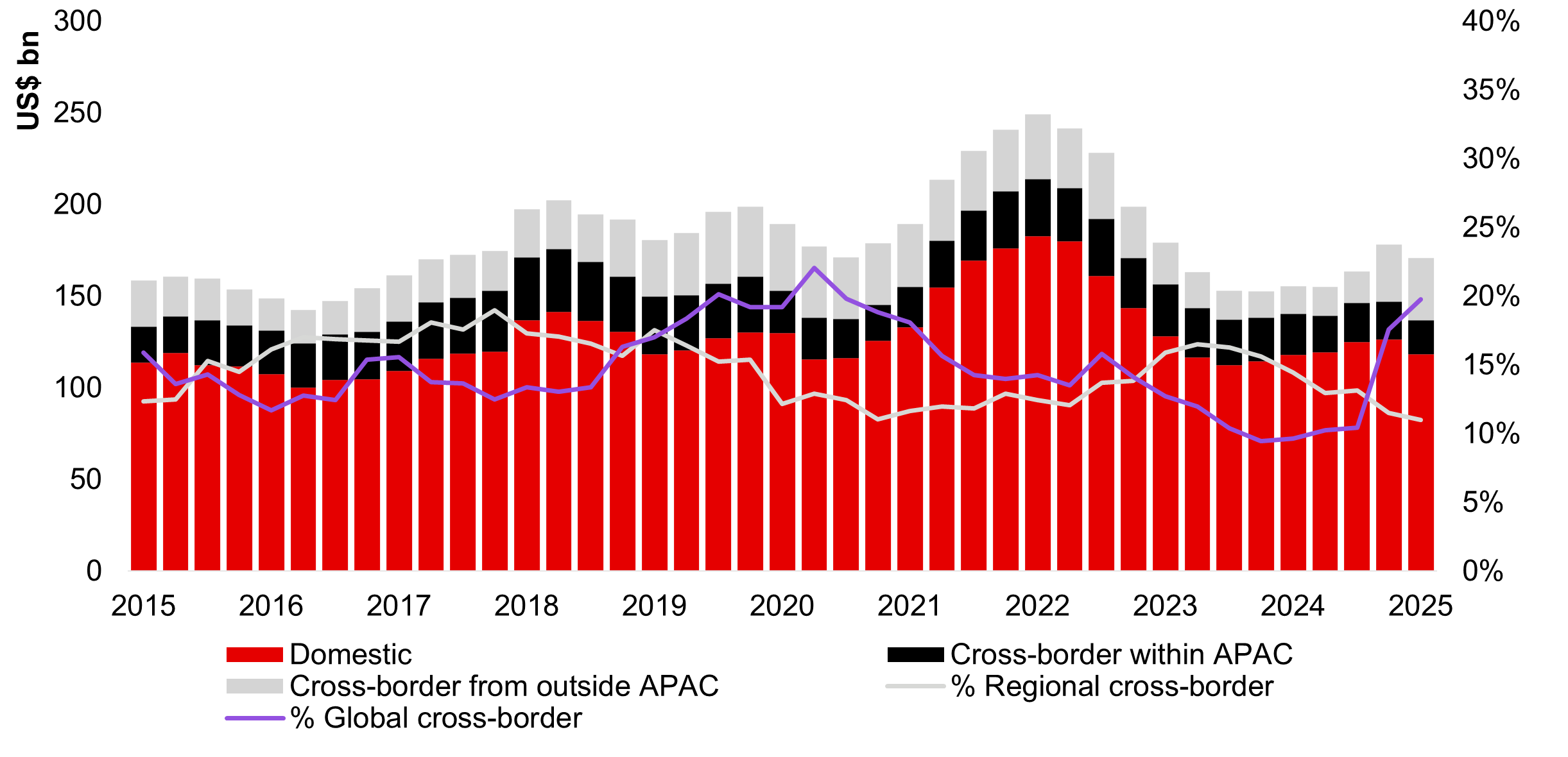

Figure 1: APAC Real Estate Investment Volume* by Source of Capital

Source: MSCI Real Capital Analytics, May 2025.

- Growing interest from investors outside APAC. Cross-border investments accounted for 31 per cent of investments in APAC in Q1 2025 based on a four-quarter rolling view, the highest level since Q4 2020; notably, capital flows from investors headquartered outside the region accounted for 20 per cent share of total investments in the quarter, up from 18 per cent in Q4 2024 and 10 per cent in Q1 2024

- Japan remained in vogue. Japan remained as APAC’s strongest performer in terms of investment activity in Q1 2025, with Tokyo ranking as the most active metro across the region based on MSCI RCA data. Backed by robust leasing market fundamentals (especially in the office and multifamily residential sectors), transaction activity was driven by several large-scale acquisitions e.g., Tokyo Garden Terrace Kioicho, Tokyu Plaza Ginza and Akasaka Plaza Building, of which many were led by foreigner investors

- China stimulus shaping up. There have been several developments with regard to China’s stimulus efforts which we are of the opinion will be a major determinant of how the Greater China real estate markets will trend going forward amid the escalating trade war between the US and China.

Notably, the Government Work Report (National People's Congress 2025) in March 2025 set the GDP growth target for 2025 to be “around 5 per cent”, as well as a record high budget fiscal deficit ratio at 4.0 per cent of GDP, surpassing levels recorded in the pandemic era. More support schemes for consumption (through a 30-point plan), social welfare and cultivating frontier technologies were also unveiled - Breadth of China’s fiscal support was wide. There was a doubling of support for the consumer goods trade-in scheme, more support for large construction projects of strategic importance and an increase in the Special Local Government Bond quota over last year’s, primarily to be used for investment, land acquisition, purchasing existing commodity housing, and settling local government arrears. There were also efforts to accelerate the legislation for a Private Economy Promotion Law to support ongoing technology innovation and adoption e.g., Artificial Intelligence developments

- Monetary easing also featured prominently. The People’s Bank of China announced a 10bp policy rate cut and a 50bp cut on the Reserve Requirement ratio in May 2025. It also announced easing measures for other interest rates such as lower relending rates for structural monetary tools and the pledged supplementary lending rate by 25bp. According to HSBC Global Research, these tools collectively have the potential to add RMB2.1trn of additional liquidity to the system

- Recovery in China real estate remains nascent. While there have been more meaningful policy maneuvers from the government, the commercial real estate market in China remains subdued as it continues to grapple with weak liquidity and investor sentiment, as well as lacklustre leasing market fundamentals (especially in the office sector). On a more positive note, there were some encouraging signs – year-to-date high-end residential sales in China remained relatively strong, while land sales momentum seems to be building up1

- Sharp decline in Hong Kong’s interest rates. The 1-month Hong Kong Interbank Offered Rate (HIBOR) rate fell significantly from 4.2 per cent at the start of the year to 0.55 per cent as of 10 June 2025, and this was mainly driven by a spike in demand for the HKD amid heightened Initial Public Offering (IPO) activity and upcoming dividend payouts in the Hong Kong stock market. This has, so far, had some positive impact on mainly the residential sector in terms of sales at some new launches and in the secondary market

- Notable office sale in Hong Kong despite its challenging market circumstances. While Hong Kong continued to perform weakly amid subdued liquidity and investor sentiment, April 2025 saw the one of the largest office transactions since early 2024 – this was namely the sale of the top nine floors of One Exchange Square (Levels 42 to 50) by Hong Kong Land to the Hong Kong Exchanges and Clearing Limited for a total consideration of HKD 6.3bn

- Understated resilience in Singapore. While the interest rate cut cycle pause in the US and global trade war have created uncertainties for Singapore’s open economy and real estate investment market, there have been several large-scale transactions over the past few months following a relatively muted start to the year e.g., Northpoint City South Wing (suburban shopping mall), 9 Tai Seng Drive (a data centre) and 5 Science Park Drive (business park development) and South Beach (50.1 per cent interest of a mixed-use integrated development). There were also several major conservation shophouses sold in April 2025 i.e., 21 Carpenter and Duxton Reserve Singapore, Autograph Collection

- Renewed interest in the living sector. While interest in the living sector has been moderating since H2 2024, a reversal of this trend was observed since the start of 2025. This was mainly driven by investors steering away from cyclical sectors such as office and industrial & logistics amid the heightened trade tensions, in favour of sectors that are less dependent on the external environment. Based on MSCI RCA data, apartment and senior housing & care acquisitions rose by 4 per cent and 13 per cent on a YoY basis in Q1 2025 respectively. Japan living volumes were noted to have risen by 16 per cent YoY in Q1 2025 according to JLL, with several portfolios transacted in Tokyo

- Major living transactions in established APAC markets. Most of the living investments in APAC were in well-established living markets. Apart from several student accommodation deals in Australia including Greystar’s acquisition of a USD1.0 bn portfolio from Wee Hur Holding and GIC, Japan saw Warburg Pincus acquiring the largest share house2 portfolio (Tokyo Beta) in the country in April 2025 while Singapore witnessed the sale of the Avery Lodge foreign worker dormitory portfolio (over 20,000 beds) to Bain Capital and several mid-sized serviced residences/ co-living deals in the past four months

1 Based on data from China Real Estate Information Corp, land sales in the first five months of 2025 were 55 per cent higher on a YoY basis in Hangzhou, Beijing, Shanghai, Chengdu, Shenzhen and Guangzhou (China’s top six cities). 2 In Japan, this refers to a co-living space where multiple tenants share common facilities e.g., kitchen, living room, and bathrooms, while having their own private rooms. Spanning across 1,195 assets and amounting to 16,192 rooms, the portfolio accounts for more than half of the share house market in Tokyo.

What was concerning?

Downside risks are intensifying

- Expecting the unexpected. Our assumptions over the previous two quarters with regard to the trajectory of Asia real estate was largely premised on the grounds that there would be greater clarity in both the US administration’s tariff direction and China’s stimulus position and unfortunately, this has not been the case. The renewed bout of uncertainty and volatility has affected investor sentiment profoundly and this has been the most apparent in the industrial & logistics sector which saw investment volume decline the most significantly (-37 per cent YoY) compared with other sectors

- Hong Kong remains one of the most challenging markets in the region. Softness persisted across Hong Kong’s capital and leasing markets in the first five months of 2025. Coupled with the oversupply situation in the office sector, investors and occupiers, by large, continued to be cautious which impacted on overall demand. Demand for prime warehouses also moderated considerably despite performing resiliently over the past few years, amid ongoing US-China trade tensions and a slowing global economy.

The changing fortunes for the city’s industrial & logistics sector have been sobering – based on data from CBRE, warehouse vacancy rate which at some point during the pandemic was below 2 per cent, has since risen to over 10 per cent in Q1 2025. With the current tariff situation, the industrial sector is likely to come under more pressure in the coming quarters. Moreover, distressed sales continued to dominate investments in Hong Kong. Financially stressed assets continued to account for a large proportion of overall investment sales – 74 per cent in Q1 2025 versus 56 per cent in Q4 2024 according to CBRE; the emergence of such ‘value buy’ opportunities may eventually help stimulate investment activity over time

What do we expect?

Unsurprisingly, the operative word going forward is ‘uncertainty’

- The heightened global downside risks and uncertainties, the prospect of weaker economic growth, the rising possibility of stagflation and interest rate volatility, are likely to impair APAC’s real estate market conditions in the short term especially in terms of liquidity

- While the world has hurtled head on into a “Trump 2.0” scenario, the events that have transpired over the recent months brings us to the view that there still remains little clarity of the way forward for APAC’s real estate markets and in particular for Greater China

- On a brighter note, there may be an accelerated “flight to safety” as we enter this renewed stretch of Volatility, Uncertainty, Complexity and Ambiguity (VUCA), which could see investors, especially private wealth capital, gravitate towards markets and investment asset classes which have proven to be stable and safe

- In the meantime, we remain cautiously hopeful for more green shoots to take root in Greater China given a combination of factors, including a new home supply squeeze, a lower-for-longer rate outlook, along with credit normalisation. Additionally, the Hong Kong IPO market has shown remarkable momentum in Q1 2025 according to KPMG – six IPOs raised over HKD1 bn in 2025 Q1, compared to just one during the same period in 2024, and this may have some positive impact on the real estate market over the next few quarters

Source: HSBC Asset Management, June 2025. The views expressed above were held at the time of preparation and are subject to change without notice. This information shouldn't be considered as a recommendation to invest in the specific country mentioned. For informational purposes only and should not be construed as a recommendation for any investment product or strategy. The commentary and analysis presented in this document reflect the opinion of HSBC Asset Management on the markets, according to the information available to date.

Important Information

For Professional Clients and intermediaries within countries and territories set out below, and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation, and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets. Investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

This document provides a high-level overview of the recent economic environment. It is for marketing purposes and does not constitute investment research, investment advice nor a recommendation to any reader of this content to buy or sell investments. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination.

All data from HSBC Asset Management unless otherwise specified. Any third party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group). The above communication is distributed by the following entities:

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- in Bermuda by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- in Chile: Operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Further information may be obtained about the state guarantee to deposits at your bank or on www.sbif.cl;

- in Colombia: HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- in France, Belgium, Netherlands, Luxembourg, Portugal, Greece by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- in Germany by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- in Hong Kong by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This video/content has not be reviewed by the Securities and Futures Commission;

- in India by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- in Italy and Spain by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- in Malta by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- in Mexico by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- in the United Arab Emirates, Qatar, Bahrain & Kuwait by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Securities and Commodities Authority in the UAE under SCA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence

- in Peru: HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- in Singapore by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- in Switzerland by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- in Taiwan by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- in Turkiye by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations

- in the UK by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- and in the US by HSBC Global Asset Management (USA) Inc. which is an investment adviser registered with the US Securities and Exchange Commission

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy

Copyright © HSBC Global Asset Management Limited 2025. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Global Asset Management Limited.

Content ID: D046902_v1.0 ; Expiry Date: 30.06.2026